When insurers think about motor risk, they often focus on who is driving and how they usually behave. But large-scale telematics data tells a different, more actionable story – one that challenges some of the most common assumptions in motor insurance:

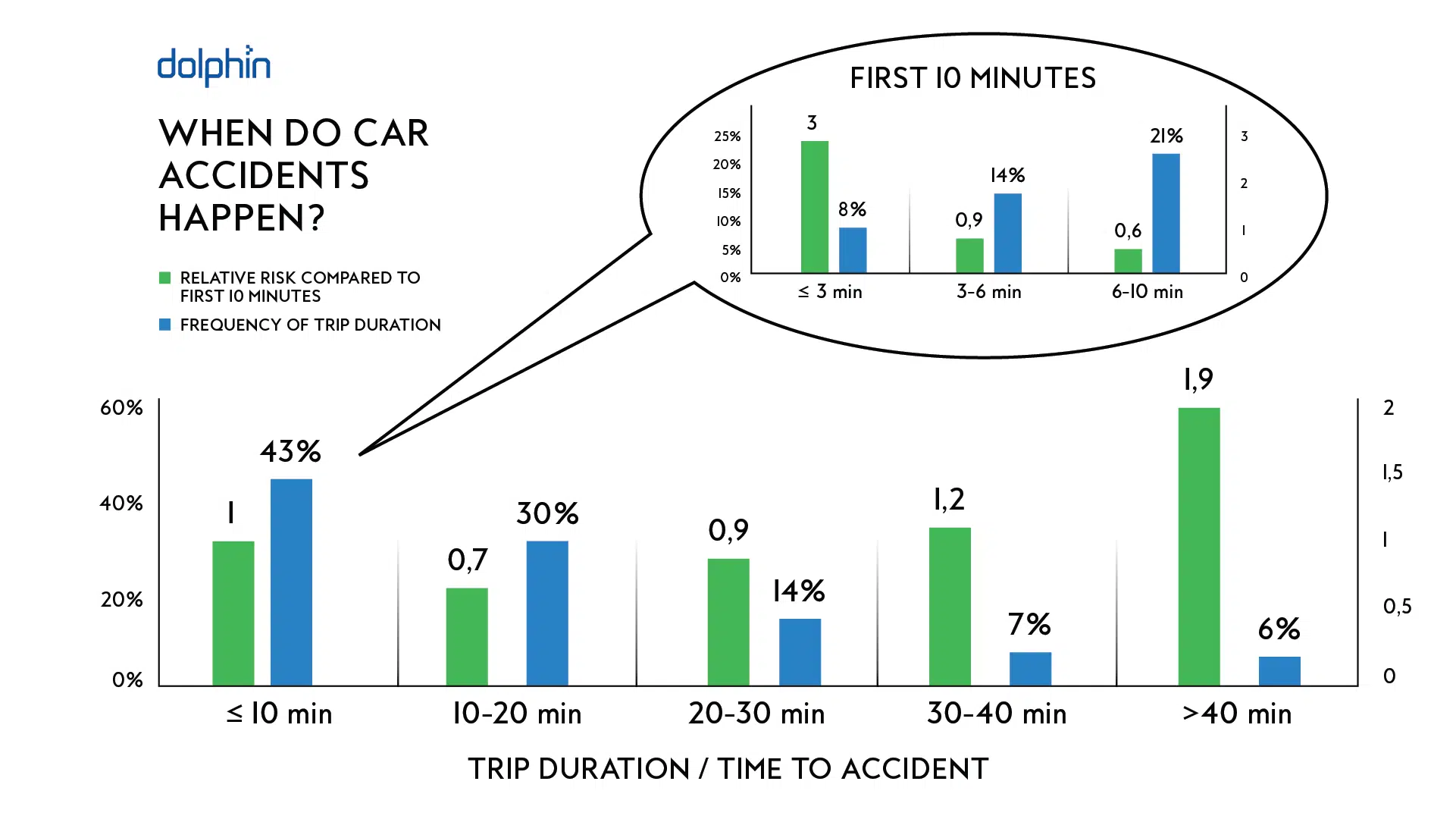

One quarter of all car accidents happen within the first three minutes of a trip.

This insight isn’t just statistically interesting. It fundamentally changes how risk should be understood, prevented, and managed.

At Dolphin Technologies, we’ve analyzed the driving behavior of tens of thousands of drivers across millions of trips, linked to verified accident events rather than proxies or simulated incidents. The result is clear: risk is highly situational – and the very beginning of a journey is one of the most underestimated danger zones.

Why the first minutes are so risky

At first glance, the start of a trip seems harmless. Drivers know the route, speeds are often lower, and distances are short. Yet data consistently shows the opposite.

Several factors combine to make the first minutes disproportionately dangerous:

- Overconfidence close to home: Familiar surroundings reduce perceived risk, leading to lower attention.

- Incomplete mental focus: Drivers are often still distracted – adjusting music, navigation, messages, or conversations.

- Short trips ≠ low risk: Brief journeys are frequently underestimated, even though accident probability is high.

- Context switching: Drivers transition from daily activities into traffic without a clear cognitive reset.

This explains why traditional models – built around annual mileage, demographics, or vehicle type – miss a critical part of the risk picture.

From averages to moments that matter

Classic underwriting models are excellent at describing average risk. But accidents rarely happen in average situations.

They cluster around specific moments and contexts, such as:

- The first minutes of a trip

- Driving under stress or time pressure

- Certain road types (urban and rural versus highways)

- Long journeys and fatigue peaks

Telematics allows insurers to move beyond static assumptions and understand when risk actually materializes.

This is where a modern, behavior- and exposure-based approach becomes essential.

Exposure matters as much as behavior

Driving behavior (speeding, harsh braking, distraction) is only part of the story. Equally important is exposure to risk – how, when, and where a vehicle is used.

For example:

- Short trips carry a significantly higher accident probability

- Urban and rural roads are materially riskier than highways

- Long trips dramatically increase fatigue-related risk

These factors are invisible in traditional pricing models, yet they strongly correlate with claims frequency.

Understanding exposure transforms raw telematics data into actionable risk intelligence.

Turning insight into prevention

Knowing that the first minutes of a trip are high-risk is only valuable if it leads to action.

Modern telematics enables insurers to:

- Prepare contextual warnings before or after a trip – never while driving

- Adapt coaching and communication to high-risk moments

- Educate drivers about hidden risks like short trips

- Support safer choices before risk escalates

Instead of reacting after an accident, insurers can become proactive risk partners in everyday mobility.

A smarter layer for underwriting and prevention

At Dolphin Technologies, these insights feed directly into solutions like MOVE Score, which complements actuarial models with real-world usage and behavior data.

Rather than replacing existing pricing logic, this approach:

- Adds a dynamic view on exposure and behavior

- Identifies good risks within traditionally high-risk segments

- Reveals hidden risks in seemingly low-risk portfolios

- Preserves strict privacy by design

The result is not just better pricing – but better prevention.

Rethinking motor risk

Risk is not evenly distributed across a trip – and the first minutes matter more than most models assume.

By focusing on when accidents happen, not just who is insured, insurers unlock a new level of precision, fairness, and impact.

Telematics makes this shift possible. Data makes it measurable. And prevention makes it valuable – for insurers, drivers, and society alike.